The federal budget has set off a lot of media talk, particularly in relation to how the proposed measures relate to the taxation of trusts, including Testamentary Discretionary Trusts (TDTs) in Wills.

In short, there are still potentially significant benefits in continuing to include TDTs as part of your estate planning strategy.

5 Points why TDTs are still useful

Here are 5 points that we trust will help clarify why TDTs are still useful:

1. The latest federal budget has not affected the strong asset protection afforded by Testamentary Discretionary Trusts (TDTs) for your beneficiaries in your Will.

TDTs remain a more protected way for your beneficiaries (for example, your children) to hold their inheritance compared to holding it in their own name, particularly if there is a risk of your child going through a relationship breakdown or bankruptcy. There is also a greater chance of inheritances being preserved for your grandchildren where there is a TDT in the Will.

2. The federal budget did not change the income splitting availability of TDTs, nor did it introduce a 30% ‘death tax’ on inheritances.

It simply introduced a tax floor underneath the income splitting of 30% on the trust income for each beneficiary. Also, it is only the income earned from the inheritance that will be taxed at 30%, not the inheritance itself.

Here are three examples of where a TDT is not going to affect the tax outcome or will result in a favourable tax outcome:

-

-

Where a beneficiary earns $45,000 – $135,000 a year (for example from their employment) – there is no tax difference to the income they receive from the TDT since the budget update.

-

Where a beneficiary earns over $135,000 a year or more, they are paying a marginal tax rate of 37% to 45% (plus the medicare levy) on any trust income earned, so the income splitting in the TDT to beneficiaries on a lower tax threshold (such as grandchildren) is still going to give them a tax saving.

-

The changes to the capital gains tax (CGT) are likely to result in greater taxes being levied on assets when they are eventually sold. If the asset is held in a TDT then any capital gain made by the TDT provides tax opportunities for splitting the gain across several beneficiaries within the TDT (such as grandchildren), potentially resulting in tax savings.

-

See the example below for some real life calculations based on the new tax.

3. The proposed changes to Capital Gains Tax (CGT) do not impose a 30% ‘death tax’ on assets in an estate.

The proposed changes to CGT do not impose a 30% ‘death tax’ on assets in an estate. Inheritance assets passing to beneficiaries remain exempt from CGT (except in certain limited cases). So importantly, when a Willmaker dies, their assets (property and shares for example) can typically pass into a TDT without triggering any CGT.

What has changed is the calculation of CGT on assets once they are sold post 1 July 2027 and the new rules will apply in the same way, whether the asset is held personally or in the TDT.

4. The legislation has not been confirmed or the details worked out.

The tax changes to TDTs have been put forward in the budget but often as the government works through the details, they amend their initial stance. This happened recently with the government’s reversal of their original stance to tax unrealised capital gains in self-managed superfunds after public debate.

Placing a minimum 30% tax on vulnerable beneficiaries in TDTs (such as minors and low-income earning beneficiaries) is placing a tax penalty on those recipients. Extensive lobbying is taking place from legal, financial and accounting groups to amend the tax as it applies to TDTs.

It is also worth remembering that governments change and the tax treatment of TDTs could subsequently be amended.

5. TDTs remain a strong estate planning strategy for your family.

Inclusion of TDTs in Wills is an important consideration because if TDTs are not drafted into a Will, your beneficiaries will not have access to one. Estate First TDT Wills typically include an ‘opt out’ provision so that beneficiaries have a choice at the time whether to take the TDT or not

Example of the federal budget impact on TDTs

Scenario:

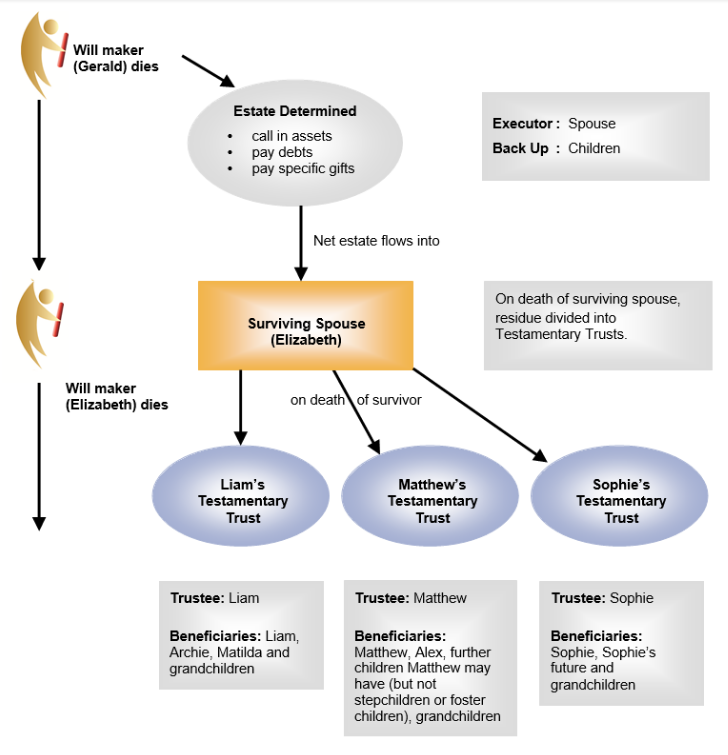

Gerald (70 years of age) and Elizabeth (65) see us. They have 3 adult children, Liam (38), Matthew (34) and Sophie (32).

Gerald and Elizabeth’s assets total $3,000,000, comprising of:

- Their main residence worth $1,500,000

- Shares worth $500,000

- Two pension accounts totalling $700,000

- Cash at bank $300,000.

Gerald and Elizabeth see Estate First and put TDTs into their Wills for each of their adult children.

Liam:

- Liam earns $125,000 (excluding super) per year from his job.

- Liam has 2 young children, Archie (10) and Matilda (6).

- Liam is in a stable relationship with his wife.

Matthew:

- Matthew works part time and makes $45,000 (excluding super) per year.

- Matthew has 1 child, Alex (5).

- Matthew is divorced. However, Matthew has a new defacto partner of about 2yrs whom Gerald and Elizabeth are concerned about. Matthew’s partner has 2 children of her own from a previous relationship.

Sophie:

- Sophie is a doctor, and earns $160,000 per year (excluding super).

- Sophie is married but has no children. Sophie plans to have children in the future.

Gerald passes away in 2028 leaving everything to Elizabeth. Elizabeth passes away 3 years later in 2031.

Each TDT for Liam, Matthew and Sophie earns $50,000 of income (i.e. a 5% return on the $1,000,000 of capital in each TDT), from dividends, rental returns and interest.

Please note that for the below examples, we have based the tax as at 2025-26 tax rates, and not included medicare levy or low income tax offsets. We have also assumed there is no other income (e.g. from investments) for each of the children. The information in this article is accurate as at 20 May 2026 and is subject to change based on modifications to the government’s proposed budget measures.

Will Structure

The Will Structure for Gerald and Elizabeth looks like this:

Liam’s Tax Position

Comparison

| Liam – No TDT in Will | Liam – TDT in Will (Post Budget) | Potential TDT Saving |

| Tax = $17,800 | Tax = $15,000 | $2,800 |

Explanation

If Liam did not have a TDT in the Will (or if he decided to ‘opt out’ of the TDT and take his inheritance outright), then his tax would be $17,800 (avg tax rate of 35.6% on $50,000), calculated as:

- Liam pays tax on the investment income at his top marginal tax rate.

- Income from his job is already $125,000

- Liam adds $50,000 from his investments taxed at:

- $125,000 – $135,000 at 30% = $3,000 tax

- + $135,000 – $175,000 at 37% = $14,800 tax

If Liam took his inheritance in a TDT in the Will, then his tax could be $15,000 (avg tax rate of 30% on $50,000), calculated as:

- TDT pays 30% flat tax on income = $50,000 x 30% = $15,000

- Liam distributes half of the income to Archie and half of the income to Matilda to pay for education, maintenance, and support.

- Archie and Matilda have no other income and so there is no top up tax for them.

- Note: Liam can pay income to himself for his own needs. He would only pay the top up tax (i.e. $2,800).

Asset Protection

In addition to the tax saving in this example, there is also an asset protection perspective. Gerald and Elizabeth want Liam’s money to be held on trust for Archie and Matilda (Liam’s children) if Liam passed away. Should something happen to Liam whilst he is still young, his wife may re-partner and have another family, meaning that any money left to Liam’s wife may not end up with Archie and Matilda.

By structuring Liam’s inheritance in a TDT, should anything happen to Liam, the money is held automatically on trust for Archie and Matilda.

Matthew’s Tax Position

Comparison

| Matthew – No TDT in Will | Matthew – TDT in Will (Post Budget) | Potential TDT Saving |

| Tax = $15,000 | Tax = $15,000 | $0 Difference |

Explanation

If Matthew did not have a TDT in the Will, then his tax would be $15,000, calculated as:

- Matthew pays tax on the investment income at his top marginal tax rate.

- Matthew’s part time job earns him $45,000 per annum.

- Matthew adds $50,000 from his investments taxed at:

- $45,000 – $95,000 at 30% = $15,000 tax

If Matthew took his inheritance in a TDT in the Will, then his tax would be $15,000 calculated as:

- TDT pays 30% flat tax on income = $50,000 x 30% = $15,000

- It does not matter if Matthew distributed the income to himself or his son Alex, as both Matthew and Alex do not have a marginal tax rate above 30%. In other words, there is no tax difference between a TDT and taking it outright.

Asset Protection

Whilst there may not be a tax saving to Matthew in taking a TDT, there is still nonetheless an asset protection advantage for Matthew, as he has:

- A relatively short term defacto spouse; and

- Step-children (from his defacto).

Assets in the TDT for Matthew provide him with greater protection from forming part of a potential property settlement should Matthew split with his partner, compared to him holding the inheritance outright.

Further, assets in the TDT on Matthew’s death are held on trust for his son Alex (not Matthew’s stepchildren), and this trust is not something that Matthew’s partner or stepchildren can claim in a family provision claim (with the exception of NSW and notional estate considerations).

Sophie’s Tax Position

Comparison

| Sophie – No TDT in Will | Sophie – TDT in Will (Post Budget) | Potential TDT Saving |

| Tax = $20,500 | Tax = $15,000-$20,500 depending | $0-5,500 Difference |

Explanation

If Sophie did not have a TDT in the Will, then her tax would be $20,500, calculated as:

- Sophie pays tax on the investment income at her top marginal tax rate.

- Sophie’s salary is $165,000 per annum.

- Sophie adds $50,000 from her investments taxed at:

- $165,000 – $190,000 at 37% = $9,250 tax

- + $190,000 – $215,000 at 45% = $11,250 tax

If Sophie took her inheritance in a TDT in the Will, then her tax could be $15,000, calculated as:

- TDT pays 30% flat tax on income = $50,000 x 30% = $15,000

- If Sophie by the time this TDT came into play had a child/ren, then she could utilise their tax brackets and not need to pay any further tax.

- If Sophie did not have children, she could distribute to herself (in which case there would not be a difference compared to taking it outright). Sophie could also look to amend the beneficiary list to include her spouse if he was on a lower tax bracket (noting that it weakens the asset protection of the TDT).

Asset Protection

Sophie’s profession as a doctor means that she has a higher risk of being personally liable in certain circumstances. Assets in Sophie’s TDT are not held by her personally, meaning that if Sophie was personally sued, the assets in the TDT form a greater protection from creditors.

Summary

In short, in most situations, there will still be a tax saving in having the inheritance in a TDT, albeit a smaller tax saving then what it may have been prior to this budget.

In addition, TDTs remain the premium vehicle for intergenerational wealth transfers, giving inheritances the best chance to preserve your family’s wealth for children and grandchildren.

Contact us for more information

Estate First Lawyers are experts in estate planning law. We can advise you on all aspects of your inheritance planning, including the best options available to you in light of the new budget measures. We are also happy to review your existing estate plan to ensure that it provides the optimum security and tax effectiveness for your particular situation.

Please get in touch with our client care team today on 1300 132 567 or email [email protected].

- The information in this article is based on the information to hand from the federal government regarding the proposed budget measures as at 20 May 2026. Some details are yet to be issued or worked through, so our worked examples may change as further information is released. The examples in this article have been prepared for educational and general information only. It should not be relied on as (or in substitution for) legal, accounting, financial or other professional advice.

- Liability limited by a scheme approved under professional standards legislation.

- Republication of this article without the Author’s written consent is prohibited.

Article written by Ann Janssen, Josh Philo and Sam Janssen