This article was written by Ann Janssen and Sam Janssen

There has been a lot of talk recently about section 100A[1] and how it impacts trust distributions in discretionary trusts (such as family trusts, and testamentary discretionary trusts in Wills).

However, section 100A has been in the legislation for decades and there is no change to its rules. It is a tax avoidance provision and the ATO has recently provided more clarification, or at least its own interpretation, on how this provision applies to certain distributions made by Trustees of discretionary trusts to the beneficiaries of the trust.

Before we look at how s100A works in this regard, let’s do a refresher on how distributions in a discretionary trust work.

How income distributions to beneficiaries in a discretionary trust work

One of the benefits of a trust is the ability to split income earned by the trust amongst the various beneficiaries named (either specifically or as a class) in the trust deed. The Trustee declares the amount of income to be distributed and to whom, prior to the end of each financial year, as part of the trust’s tax return and financial reporting. Distributions are then taxed in the hands of the recipient beneficiaries, at their respective marginal tax rates. Of course, distributions to beneficiaries with lower tax rates means less tax paid on the trust income overall, and as the beneficiaries are often family members, there is a tax saving to the family group. Whilst minors (that is, children under the age of 18) receive a tax-free threshold of only $416 in family trusts, in testamentary discretionary trusts their tax-free threshold matches the adult threshold of $18,200, and the threshold increases if LITO and LMITO apply.[2]

Whilst the income distributions must be ascertained each year and taxed, the cash does not have to be physically paid out of the trust to the beneficiaries. Unless the beneficiary demands payment, the Trustee can decide to keep some or all of the cash (representing the distribution) in the trust. That beneficiary can call on the money at any time (that is, they are presently entitled to the trust distributions owing to them). These sums are technically referred to as ‘unpaid present entitlements’ (UPEs) and they appear as a liability on the trust’s balance sheet. This allows the distributions to be retained within the trust and used for further investment, or loaned to others, for their use and benefit.

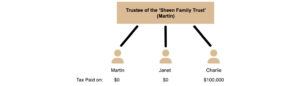

Let’s take an example of the Sheen family:

The Sheen family include the parents, Martin and Janet. Their son Charlie is a university student who earns $15,000 a year from his part-time job as an extra in commercials. Charlie’s parents are both on a very high income (taxed at the highest marginal rate of 45% + 2% Medicare levy).

The trust has earned $100,000 of income from its various investments for the financial year.

From a tax perspective, it is beneficial for Martin, as the Trustee of the Trust, to distribute all of the income to Charlie so that it is taxed at Charlie’s much lower marginal tax rate. If the trust does not physically pay out the cash to Charlie, Charlie becomes presently entitled to the cash (i.e. he can call on it at any time).

What is s100A and all the ‘fuss’ about?

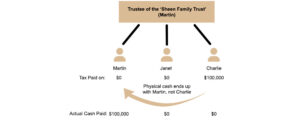

The ATO’s issue is where the Trustee makes a trust distribution to a beneficiary (such as Charlie in the above example) to get the lower tax rate, but another person, such as Charlie’s father or mother, actually receives the cash.

The ATO sees this as a scheme to avoid tax and will start to crack down on them. Section 100A will be an issue where:

-

-

-

- A beneficiary (e.g. Charlie) has been made presently entitled to income (that is, the trust has declared a distribution to Charlie); and

- Charlie is not under a legal disability (for instance, he is over 18, not bankrupt or suffers from loss of capacity); and

- The present entitlement (i.e. the trust distribution) is part of a ‘a reimbursement agreement‘ (note: this simply means that there is some understanding that the benefit given to Charlie as beneficiary will somehow end up with someone else (in our example, that is Martin); and

- The actual benefit is given to someone else, say Martin; and

- The agreement is not part of an ‘ordinary course of family / commercial dealing’; and

- A purpose of this arrangement is to reduce tax.

-

-

Using the above example, the ATO’s interpretation of s100A would start to crack down on situations that look like this:

To clear up a misnomer straight away, the good news is that s 100A does not apply to trust distributions to children under 18.

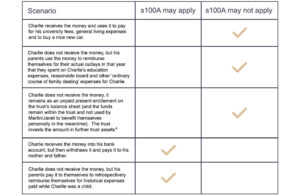

Examples of what would and would not be caught by s100A

Taking our example of the Sheen Family Trust, the following table highlights some examples where s100A may or may not apply to the transaction.[3]

If s100A applies to the Sheen Family trust, the $100,000 trust distribution would not be taxed at Charlie’s marginal tax rate, but at the true recipient’s marginal tax rate, which in this case is 47%…. Ouch.

What is the impact on Testamentary Discretionary Trusts (TDTs) in Wills?

The good news is that TDTs remain an advantageous tax planning vehicle in Wills for your clients because:

-

-

-

- s100A does not apply to beneficiaries who are children under 18.

This means that if you leave an inheritance to your adult child in your Will, once you pass away, your child can use the TDT to make tax concessional trust distributions to their minor children (your grandchildren). Trust distributions to minors (in TDTs, not family trusts) enjoy a tax-free threshold yearly of $18,200, and more with the current low and middle income tax offsets. Remember, minors do not have to be your children/grandchildren, they can be any other minors that you name as a potential beneficiary in the TDT terms (such as nieces/nephews etc…). This money can remain in the TDT[5] or be used towards the costs of raising the child, such as education expenses, maintenance costs or used to reimburse say, the parent or guardian who physically outlaid those costs. This can be done each financial year up to the child turning 18. - Income splitting amongst children who are over 18.

Your children (or other beneficiary in your Will) for whom you have provided a TDT will have tax options not otherwise available to them if you had left them their inheritance outright. This includes splitting the income that the TDT earns off the inheritance amongst their own children (your grandchildren) who are over 18, as well as other adults named in the TDT, as your child, in their discretion, decides at the time. As long as the rules of s100A are not violated (see above table for some examples), your child’s TDT will provide a lower tax solution. - Income splitting amongst other beneficiaries.

One of the great advantages of discretionary trusts is the ability to distribute income across a range of beneficiaries who pay tax at their personal marginal rate. There may still be advantages in splitting income amongst other beneficiaries within a trust, such as to a low income earning spouse (being mindful of how that impacts the asset protection of the trust in a family law dispute), or to a corporate beneficiary (i.e. a ‘bucket company’, which pays a corporate tax rate of 30% rather than the highest marginal rate of tax of 45% + 2% Medicare levy).[6]

- s100A does not apply to beneficiaries who are children under 18.

-

-

Please talk to one of our estate planning solicitors to discuss this in more detail by calling 1300 132 567 or emailing [email protected]

Importance of asset protection in a TDT

It is important that we don’t lose sight of the most significant advantages of TDTs, namely its asset protection qualities.

Remember that a TDT that is well-drafted and structured, can offer a greater degree of protection for their inheritance than if you were to gift it to them outright in your Will. Scenarios where asset protection becomes important include:

-

-

-

- Relationship breakdown, separation and divorce;

- Being sued (for negligence, in business, for injury/damage to others);

- In bankruptcy; and

- To protect and preserve an inheritance for beneficiaries who are immature or otherwise not capable of managing their inheritance. Terms can be placed for beneficiaries to receive control of their TDT at a certain age, for example. In other situations, control may never pass to the beneficiary, but be managed by an independent Trustee for the TDT beneficiary’s benefit.

-

-

Conclusion

TDTs remain an important structure to utilise within a Will, both for greater asset protection as well as tax planning flexibility for your intended beneficiaries.

If you want to know more about TDTs in Wills or to have your own estate planning reviewed, then please contact one of our expert estate planning lawyers on 1300 132 567 or email us at [email protected].

Estate planning tools for our Advisers

Here at Estate First, your clients’ estate planning is our passion and focus. We value our working relationships with you as advisors and can support you in whatever way you need, including training and presentations (whether to your team or to your clients), compliance support, and tools and fact sheets (which you can use or provide to your clients). Please get in touch with us today by clicking here.

Please note that the TR 2022/D1 and PCG 2022/D1 are currently draft guidance from the ATO and are currently being subject to feedback from professional bodies and the public.

Please also note that the information provided in this article is general in nature, current as at the time of first publication. It does not constitute legal advice, should not be relied upon as if it were and should not be acted upon without first obtaining legal advice on the particular situation.

[1] Income Tax Assessment Act 1936(Cth)

[2] LITO = Low Income Tax Offset. LMITO = Low and Middle Income Tax Offset.

[3] For further examples, see TR 2022/D1 and PCG 2022/D1. The above table is provided to by way of example only – do not rely on this table when seeking to do a particular transaction – please seek your own legal and tax advice.

[4] PCG 2022/D1 may classify an unpaid present entitlement (UPE) held within the trust to fall into the ATO’s ‘blue’ category of risk (moderate risk which may be subject to the ATO’s review but are ‘less likely to attract’ their attention when compared to ‘red’ category of risk) if this UPE was converted into a loan, or forgiven or somehow used to defer or avoid tax. Please see PCG 2022/D1 for more examples on this point.

[5] But note that this will increase the UPE owing to that child which may be an issue later on in life, such as that child going through a property settlement and this UPE is an ‘asset’ that belongs to them to be divided amongst their ex-partner.

[6] Please note that s100A can apply to payments made to bucket companies in which the company then issues a franked dividend back to the trust. This arrangement is outside the scope of this article, but we refer you to TR 2022/D1 and PCG 2022/D1 for further reading on this topic.